Why PM-602-0199 Cannot Touch the EB-5 Concurrent Filing Right, and Where Real Scrutiny Will Actually Land

By: Mona Shah, Esq.

The Panic, and the Statute That Answers It

In the days since USCIS released Policy Memorandum PM-602-0199, the EB-5 community has reacted as though the in-country green card has been abolished. It has not. The memorandum recasts adjustment of status as “an extraordinary discretionary relief” and “an act of administrative grace,” and that language, pushed out the Friday before the Memorial Day weekend, was engineered to alarm. For most EB-5 investors, alarm is the wrong response, because the question the memorandum raises was answered by Congress three years ago.

The release did not go unnoticed. Within hours it drew national coverage, from the New York Times to NBC News and NPR, much of it reporting that the administration would now require most applicants to leave the country and process abroad, and that the agency had characterized a decades-old in-country process as a “loophole” it was closing. What that coverage largely passed over, and what matters most to EB-5 investors, is that Congress addressed this precise point by statute in 2022. Even the general-interest press caught the tension: reporting on the announcement noted that Congress expressly provided for adjustment of status in Section 245 of the Immigration and Nationality Act, which makes the “loophole” characterization difficult to sustain.

The right to file is not a matter of administrative grace. Congress wrote it into the statute in 2022, and a memorandum cannot unwrite it.

The right to file is not a matter of administrative grace, as the current Administration would have us believe. Congress wrote it into the statute in 2022, and a memorandum cannot unwrite it. The purpose of this alert is to separate the part of the EB-5 adjustment process that the memorandum cannot reach, which is most of it, from the narrow set of circumstances where genuine scrutiny will land. The conclusion, stated at the outset so that no client reads past it in fear, is this: the clean concurrent filer with a visa available is standing on statutory ground, not administrative goodwill.

There is an irony the global mobility industry has already seized.

There is an irony the global mobility industry has already seized. While USCIS brands the in-country green card as extraordinary relief dispensed by grace, the residency and citizenship by investment programs competing for the same capital, from Portugal and Greece to Malta and the Gulf, sell precisely the opposite: fixed criteria, defined timelines, and predictable outcomes. By recasting its own domestic pathway as a disfavored exception, the agency has handed those programs a quotable advertisement at no charge, and RCBI practitioners abroad have been forwarding the memorandum to prospective clients as confirmation of everything they have argued about American friction and unpredictability. For the EB-5 investor weighing global options, that contrast is worth keeping in view. It is also, as the statutory analysis below demonstrates, considerably overstated, because the domestic route remains far more secure than the memorandum’s tone suggests.

What Congress Did in 2022 Through RIA, INA § 245(n) and the 245(k) Exemption

The EB-5 Reform and Integrity Act of 2022, enacted as Division BB of Public Law 117-103 on March 15, 2022, did not merely tolerate concurrent processing. It codified it. Section 102(d) of Division BB amended Section 245 of the Immigration and Nationality Act in two ways. Foremost, it added a new subsection, INA § 245(n), 8 U.S.C. § 1255(n), providing that where approval of a petition under Section 203(b)(5) would make a visa immediately available to the beneficiary, the beneficiary’s adjustment application shall be considered to be properly filed whether submitted concurrently with, or subsequent to, the visa petition. Next, it brought EB-5 within the protection of INA § 245(k), striking the language that had excluded the fifth preference and inserting it among the categories that enjoy forgiveness.

The two amendments work in tandem, and both matter to the present question. Section 245(n) establishes the right to file the I-485 in the United States rather than process abroad, and it does so in mandatory terms. Section 245(k), now extended to EB-5, forgives up to 180 days of failure to maintain lawful status and up to 180 days of unauthorized employment since the applicant’s last lawful admission. Before the RIA, EB-5 was the lone employment-based category excluded from that forgiveness. Congress deliberately removed that exclusion. These are not regulatory accommodations or policy-manual courtesies. They are statutory text, recent, specific, and bipartisan.

The Filing Right Is Locked

The decisive analytical point, and the one that dissolves most of the panic, is that 245(n) and the memorandum operate at different stages of the process. Section 245(n) governs filing. The memorandum governs the exercise of discretion at adjudication. Understanding that distinction tells a client exactly how much of the memorandum can reach them.

At the filing stage, the statute is categorical. When a visa is immediately available, the EB-5 adjustment application shall be considered to be properly filed. A policy memorandum cannot direct officers to reject those filings, to treat them as improperly filed, or to hold them in abeyance, because each of those actions would contradict the statutory command. Notably, the memorandum does not even purport to do so. It does not suspend adjustment filings, and it does not direct denial of pending applications. The interim benefits that flow from a properly filed, pending I-485, employment authorization and advance parole under the governing regulations, rest on that statutory filing right and are not within the memorandum’s reach.

For the reserved set-aside investor, this is close to dispositive. Because the rural, high-unemployment, and infrastructure categories have generally carried current priority dates, a visa has been immediately available, and the concurrent I-485 has been properly filed as a matter of statute. That filing, and the work and travel authorization built upon it, sits beyond the memorandum’s authority. The investor whose unreserved category is current by country of birth stands in the same position.

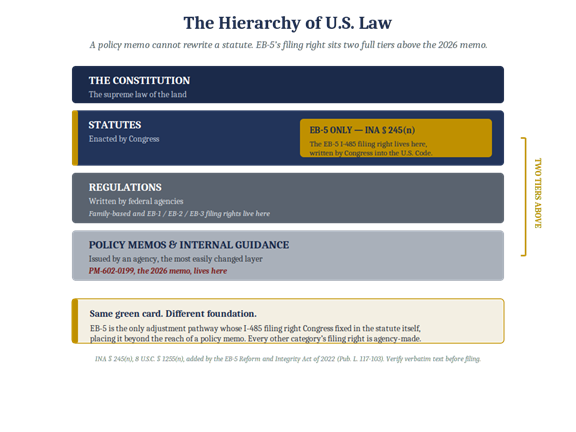

Figure 1. The EB-5 I-485 filing right is fixed by statute at INA § 245(n), two tiers above the policy-memo layer where PM-602-0199 sits. EB-5 is the only adjustment category whose filing right Congress placed in the statute itself.

Where the Memorandum Operates, and Where It Collides

Candor requires acknowledging what the memorandum can still touch. Section 245(n) made concurrent filing a statutory right, but it did not strip adjustment of its discretionary character at the moment of approval. Adjustment under Section 245(a) has always been discretionary as to the grant. The memorandum therefore operates at the grant stage, instructing officers on how to exercise that discretion, and on that ground the agency will argue there is no conflict with 245(n) at all because the statute speaks to filing while the memorandum speaks to approval.

That argument fails for EB-5 at two specific points, and counsel should press those points rather than the general proposition that adjustment remains discretionary, which it does.

Penalizing an investor for using the route Congress built for him is not the exercise of discretion. It is resistance to the statute.

Foremost is the in-country choice. The memorandum’s most aggressive instruction is that an officer may weigh against the applicant the decision to adjust in the United States rather than depart and process at a consulate. For EB-5, that instruction runs directly into the purpose of 245(n). Congress created an express, recent, EB-5-specific right to remain and adjust. Penalizing an investor for using the route Congress built for him is not the exercise of discretion, rather it can be considered to be resistance to the statute. The canon that the specific and later-enacted provision governs the general favors the investor here, because 245(n) is both more specific and more recent than the discretion cases on which the memorandum leans.

Next is the 245(k) conduct. The memorandum lists status violations and unauthorized employment among the adverse factors officers must weigh. For EB-5 investors, Congress expressly forgave up to 180 days of precisely that conduct. An officer who treats a status lapse or unauthorized work within the 180-day window as a negative discretionary factor against an EB-5 adjustment applicant is weighing as adverse the very conduct the statute commands shall not bar adjustment. That is not a permissible exercise of discretion. It is an officer acting against the text of 245(k).

Where Scrutiny Will Actually Land

The practical impact sorts EB-5 investors into three groups, and most clients sit in the first.

The lowest exposure, and the largest group, comprises those standing on statutory ground. The reserved set-aside investor filing concurrently while a visa is available is protected at the filing stage by 245(n). The investor consular processing from abroad sits outside the in-country adjustment framework entirely, since the memorandum points toward consular processing as the default rather than adding friction to it. The clean-record investor maintaining H-1B or L-1 status holds the strongest discretionary position of all, because the memorandum expressly preserves dual intent for those categories. For these clients, the correct posture is documentation and confidence, not alarm.

The moderate and genuinely relevant exposure falls on a narrower set. Sub-180-day status lapses and unauthorized employment are forgiven by 245(k), and should be documented and explained rather than feared. The investor who entered in a category that carries no dual intent, the F-1 student foremost among them, carries real preconceived-intent exposure, because a rapid transition from a temporary classification to permanent residence invites the question of immigrant intent at the time of entry. That question is answered with a contemporaneous record, not reconstructed after the fact. And the generic instruction to weigh the choice to adjust in-country technically reaches every applicant, but for EB-5 it is the collision point with 245(n) and therefore the agency’s weakest ground rather than the investor’s.

The genuine exposure, finally, is largely what it was before the memorandum. Fraud or misrepresentation, criminal conduct, status violations beyond the 180-day forgiveness window, and prolonged overstay were adverse discretionary factors before May 2026 and remain so. The memorandum sharpens the lens. It did not invent these factors, and an investor who carried this exposure last year carries no more of it today because of a policy memorandum.

The Litigation Posture

Should the agency apply the memorandum to deny an otherwise approvable EB-5 adjustment on the strength of the in-country choice or 245(k)-forgiven conduct, the challenge writes itself. The statutory argument is the strongest: a general discretion memorandum cannot narrow a specific statutory right that Congress enacted in 2022, and after Loper Bright Enterprises v. Raimondo, 603 U.S. 369 (2024), the agency defends its reading without the deference it enjoyed for forty years. The administrative-law argument reinforces it: the memorandum cites the precedent establishing that adjustment is discretionary while ignoring the Board’s own counterweight authority that discretion is ordinarily exercised in favor of an eligible applicant with no significant adverse factors. That selective citation is the textbook setup for an arbitrary-and-capricious challenge under Motor Vehicle Manufacturers Association v. State Farm, 463 U.S. 29 (1983).

One procedural feature cuts in the investor’s favor. A discretionary denial must set out, in writing, the positive and negative factors weighed and explain why the negatives prevail. For an EB-5 investor whose only negatives are the in-country choice and conduct within the 245(k) window, that written analysis becomes the record of the agency’s own error. The candid caveat is jurisdictional: review of an individual officer’s factual weighing of equities is constrained, so the stronger vehicles are the statutory and programmatic challenges rather than a quarrel with one officer’s discretion.

Recommended Action

Foremost, for clients eligible to file concurrently with a visa available, file. The statutory right to do so is intact, and delay forfeits the interim work and travel authorization that the pending application secures. Next, build the equities record into the I-485 from the outset, length of residence, family ties, tax compliance, employment, and good moral character, so that the discretionary analysis the memorandum demands is answered before it is asked. Then, for investors who entered on a non-dual-intent visa, document the absence of preconceived intent contemporaneously, because that record cannot be assembled later. Finally, for any investor carrying genuine exposure, fraud, criminal history, or status violations beyond the forgiveness window, address it directly with counsel rather than waiting for a Request for Evidence or a Notice of Intent to Deny.

Above all, do not file defensively and wait to be questioned. A capable EB-5 practitioner will build the legal argument into the filing itself rather than holding it in reserve. The application should state expressly that the concurrent I-485 is filed as of right under INA § 245(n), that any status lapse or unauthorized employment within the 180-day window is forgiven under INA § 245(k), and that the applicant’s equities warrant a favorable exercise of discretion, with each proposition supported by documentary evidence, sworn affidavits, and exhibit cross-references. An argument advanced affirmatively at filing, on the record, is far harder for an officer to disregard than one raised only after a Notice of Intent to Deny, and it positions the file as both an administrative submission and, should it come to that, a clean record for federal court review.

The memorandum was written to sound sweeping. As Abdul Arif observed “The fear that it has created has given an undue impression that all is lost – when it is not.” The statutory framework enacted by Congress tells a different story. The statute is what governs. For the EB-5 investor who reads past the rhetoric, the controlling text was enacted in 2022, it remains in force, and it says what it says. Panic is the wrong response to a memorandum that Congress already answered.